Once again, for individuals who currently have a monthly budget, you might know what you may be investing per month toward one thing instance market, resources, as well as your cellular telephone bill.

If you can’t crack your lease, you may possibly have particular convergence while using your own lease and the financial. not, that won’t last forever, which means that your monthly lease must not factor to your exactly how much domestic your can afford.

Simply how much Home Must i Manage on the people income

Before attempting to ascertain how much house you can afford, know if you might be financially prepared to purchase a house by inquiring oneself these types of concerns:

- Are We obligations-100 % free that have 3 to 6 days regarding costs during the a crisis finance?

- Should i create about a 10 percent (if at all possible 20 percent) down-payment?

- Perform I’ve adequate cash to fund closing costs and swinging expenditures?

- ‘s the family payment 25 percent otherwise less of my personal month-to-month take-family pay?

- Do i need to be able to take out an excellent fifteen-seasons fixed-rates mortgage?

- Can i pay for constant repair and tools for this household?

For folks who replied no to your of one’s over issues, now is almost certainly not just the right time to buy property. Merely married? Waiting at the least annually before buying a home, even if your money are in order. You should never are the be concerned off a property buy so you’re able to a brand name-the latest marriage, and not get a property together with your mate unless you are actually partnered!

Knowing the twenty eight Percent Code

Typically the most popular code to possess determining as much as possible pay for a home is brand new twenty eight % you to, even if lots of people are nowadays. You can buy property that will not just take anything else than twenty-eight % of one’s disgusting month-to-month income.

Such as for instance, for folks who attained $one hundred,100000 annually, it 300 online loan might be no more than $dos,333 thirty days. Now keep in mind that you to definitely prices need to security everything, including repairs, fees, insurance policies, and HOA costs. The financial institution will use a personal debt-to-income proportion to see if you really can afford that it room, and this is called the front side-end proportion.

How the thirty six Per cent Rule Varies?

Another loans-to-money ratio is known as the back end. So it ratio varies because it discusses the construction costs along with most other monthly obligations. If you have an automible commission, bank card expenses, or son service, it might be figured into the which formula.

After you incorporate the newest thirty-six percent code to the $a hundred,100000 a year income, your own monthly obligations cannot go beyond $ 3,100000 thirty day period. Now, some loan providers try a tad bit more lenient and certainly will allow you to increase up to 42 per cent, you might be wary of getting back in over your face and you will stretching your bank account to the cracking section.

It’s important to arrange for these types of expenditures, too, and that means you score a right estimate from what you are able manage centered on the monthly budget.

- Principal and desire- Dominating is the amount borrowed. Notice is the price of borrowing financing. Monthly, a particular part of the fee goes toward paying down the primary, and one region visits appeal.

- Property taxes- Possible spend assets taxes to the home, as well. Lenders create it amount to their homeloan payment, and it’s really paid back thru an enthusiastic escrow membership. Possessions taxation derive from the value of your residence

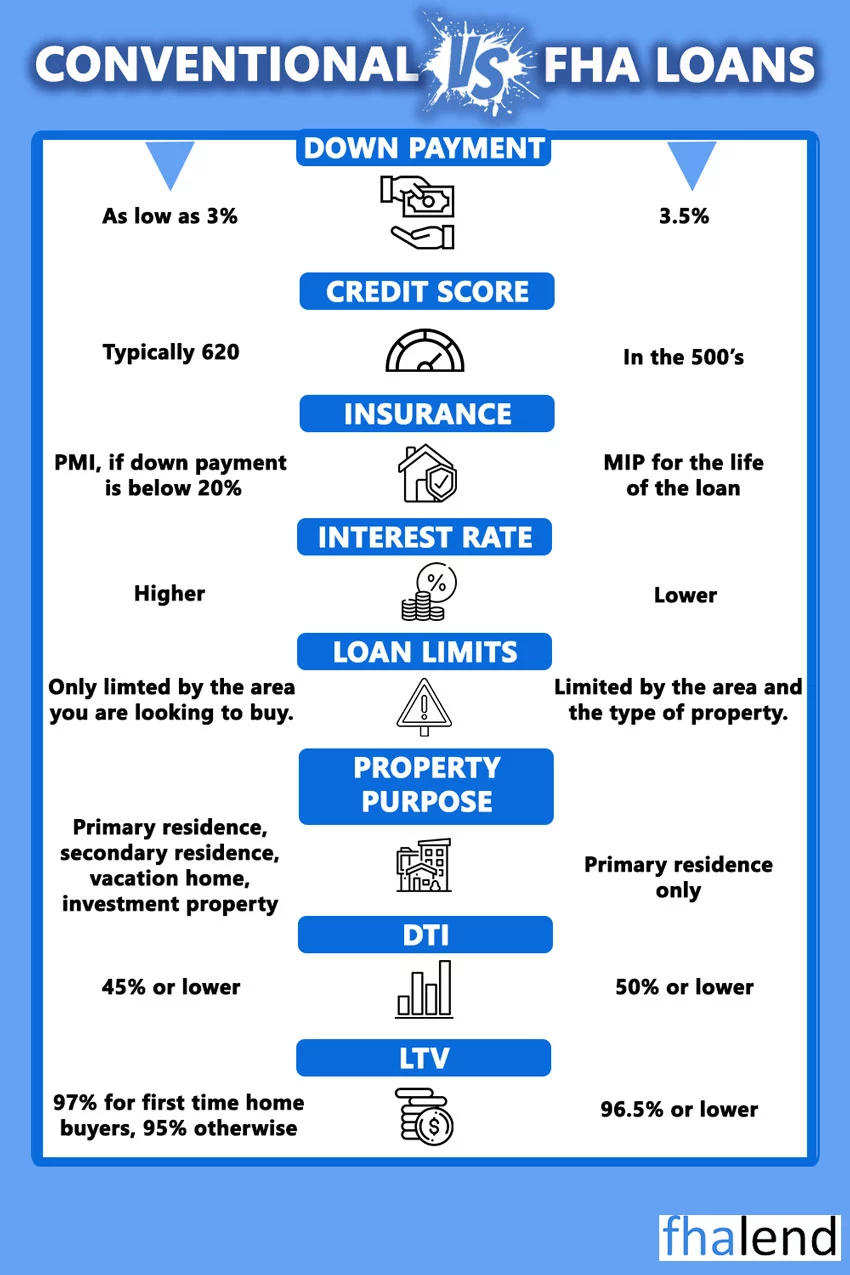

- Insurance- Homeowners insurance required once you purchase a house. That it protects the home away from injuries including thieves, fire, otherwise natural crisis. You might like to need to pay getting personal mortgage insurance policies (PMI) if you purchase a home which have below a 20 percent down. That it insurance rates protects the financial institution for many who standard towards mortgage