In business and other organizations, a budget often refers to a department’s or a company’s projected revenues, costs, or expenses. Typically, a manufacturer will have a budget for each of its manufacturing departments. Assume that the finishing department’s budget for the upcoming year is $400,000 and is expected to process 50,000 identical units of product. AccountingCoach PRO includes forms to assist in a better understanding of standard costs and their related variances. A budget is done at the macro-level of a business and guides every other financial activity, while standards are set at different micro levels/ departments in the business. It provides criteria that can be used to evaluate and compare the operating performance of executives.Essentially, Standard Costing is a technique of cost calculation and control.

Would you prefer to work with a financial professional remotely or in-person?

Budgetary Control makes side by side comparisons, and that is why periodic revisions are made in the budgets, and that is why there is no need for reporting the variances, which is absent in Standard costing. For example, the standard cost of processing all identical units in the finishing department is $8 (based on its budget of $400,000 divided by the expected 50,000 identical units). Therefore, if 4,000 units are processed, the standard cost of the company’s inventory will be increased by $32,000. In cost accounting, standard costs refer to the usual costs incurred in production.

Key differences between Standard Costing and Budgetary Control

Budget costs are estimated costs that are used only for planning or research purposes to understand the size of the company and make business decisions. Standard costing is a method of cost accounting in which a company assigns a predetermined cost to each unit of production learn bookkeping and accounting online for free or service. These predetermined costs are based on estimates of the costs of materials, labor, and overhead. The actual costs incurred during production or service delivery are then compared to the predetermined costs, and any differences are tracked as variances.

Ask a Financial Professional Any Question

This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

Ask Any Financial Question

A budget generally refers to a department’s or a company’s probable revenues, costs, or expenses. A standard generally refers to a projected amount per unit of product, per unit of input, or per unit of output. A standard is a benchmark that is established to form the basis for cost variance analysis.

Budgeting Helps You Understand Your Relationship with Money.

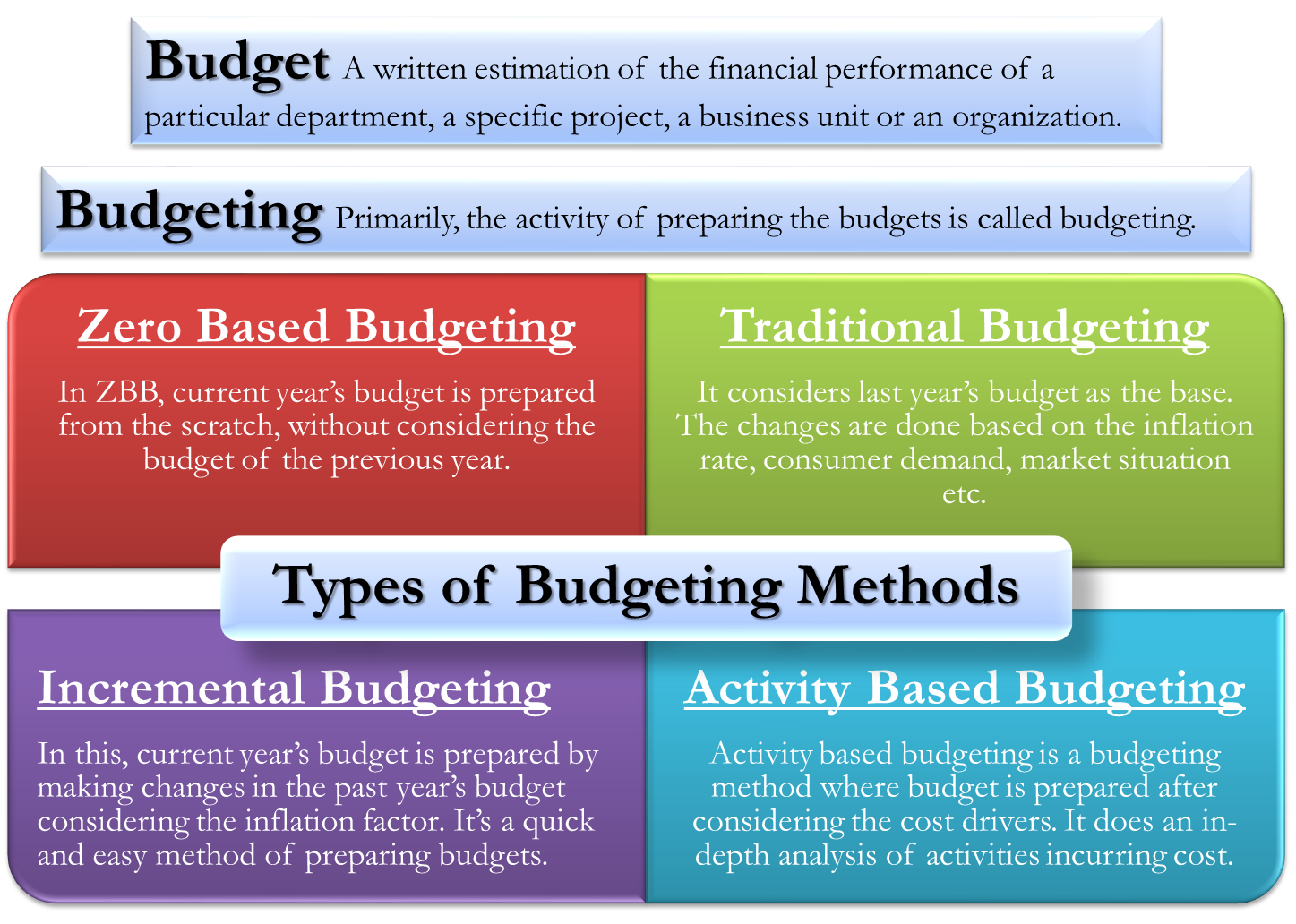

- This is a time-consuming approach, but does allow for incremental changes to the budget.

- A standard generally refers to a projected amount per unit of product, per unit of input, or per unit of output.

- The Budgetary Control system facilitates the management to fix the responsibilities and coordinate the activities to achieve the desired results.

- The control and management of cost is, therefore, one of the chief functions for all commercial entity.

- Budget costs are estimated costs that are used only for planning or research purposes to understand the size of the company and make business decisions.

- It provides criteria that can be used to evaluate and compare the operating performance of executives.Essentially, Standard Costing is a technique of cost calculation and control.

It involves setting budgets, monitoring actual results, and making adjustments as necessary. The goal of budgetary control is to ensure that resources are used efficiently and effectively to achieve the organization’s strategic objectives. In addition to this, the management can keep a check on the organizational activities by assessing the deviations, i.e. analyzing the difference between actual performance and the standard performance. Standard Costing delineates the variances between actual cost and the standard cost, along with the reasons. Whether your clients are creating a budget or trying to identify the most effective production methods, standard costs provide a useful data point.

It does not provide for any variability in the amount of units sold, price points, activity levels, and so forth. As such, a standard budget represents a single best estimate of the future performance of a business through the budgeting period. This approach works best when the business model is relatively simple, revenues rarely deviate from expectations, and expenses are highly predictable. Conversely, it functions poorly in a more fluid business environment that is more difficult to predict. The standard budget is commonly used in a centralized command-and-control environment, since it allows senior management to judge the performance of the organization in comparison to a single forecast of future results.

If it sees that difference immediately, it knows its profits are likely to be higher than usual. Similarly, if a company uses $20,000 as a standard figure for monthly labour expenses but then incurs $25,000 in payroll costs, the accounting records immediately note that 25% increase. Budgeted costs tend to overlap with standard costs, but they’re not exactly the same. In many cases, companies take the standard costs from the previous year and use them as their budgeted costs for the current year. Alternatively, businesses can use standard costs as a jumping off point to set their budgeted costs. In many situations, companies break down standard costs per unit, but they use budgeted costs for overall expenses.

Budgeting helps you track your income and expenses and paints a clear picture of the necessary amount of money you need to save or spend. One benefit of budgeting is that it helps you live within your means and device means to put your money to work in the best way possible. Whether you are financially buoyant or struggling with keeping your finances in check, budgeting is one act you should learn to do. A budget is prepared by a group of directors and board members who have to decide critically whether an item is worth spending on in the new financial year.

If a company wants to be able to create budgets, forecast cash flows, or keep expenses consistent, it needs these numbers. Explain these types of costing methods to your clients and let them know which ones they should track and use. Here, budget refers to a written financial statement expressed in monetary terms prepared in advance for future periods, containing the details about the economic activities of the business organization. While a budget refers to a forecasted list of future income and expenditures, a standard is a benchmark that determines what cost the company cannot exceed and what amount of output is considered fundamental. After necessary calculations, if the variance between the standard and the actual cost is positive, the company made progress.

For example, if a client is trying to create a budget and knows prices are going up, it can add the projected increase in materials to the standard price to create the budgeted amount. This actually means that any fixed expenses are not altered in the budget, while expenses considered to be variable will adjust in the budget, based on the actual sales generated within a budget period. The budget model may also contain some mixed costs, which contain a fixed element and a variable element; in this case, only the variable element is altered in accordance with sales levels. While standard costs can be a useful management tool for a manufacturer, the manufacturer’s external financial statements must comply with the cost principle and the matching principle. Therefore, significant variances must be reviewed and properly assigned or allocated to the cost of goods sold and/or inventories.